The year 2018 has not been very friendly toward the hedge fund industry in general, with the Eurekahedge Hedge Fund Index down 2.36% year-to-date, in contrast to how it returned 8.51% last year. The return of market volatility, combined with the escalation of the US-China trade war around the middle of the year, as well as the political uncertainties surrounding Brexit negotiation and Italy’s debt level have exerted significant pressure on the hedge fund industry. The global hedge fund industry AUM stood at US$2,364.7 billion as of November 2018, down US$82.0 billion year-to-date as fund managers recorded performance-based losses and investors fled into safer asset classes. Asian fund managers were hit particularly hard as the tariff spat between China and the US exacerbated the already growing concerns over the region’s slowing economic growth, and the Fed rate hikes weighed on Asian and emerging currencies throughout the year.

The two tables below provide the performance of the Eurekahedge indices broken down across geographic and strategic mandates over the last two years. Annualised returns of the indices are provided to represent the long-term performance of the regions and strategies.

Table 1: Regional indices performance

| Index |

2018 YTD Return |

2017 Return |

Annualised Return |

|---|---|---|---|

Eurekahedge Hedge Fund Index |

(2.36%) |

8.51% |

8.34% |

Eurekahedge North American Hedge Fund Index |

0.87% |

8.27% |

9.21% |

Eurekahedge European Hedge Fund Index |

(2.88%) |

7.15% |

6.74% |

Eurekahedge Eastern Europe & Russia Hedge Fund Index |

(6.83%) |

10.78% |

12.14% |

Eurekahedge Asia ex Japan Hedge Fund Index |

(7.73%) |

20.75% |

9.70% |

Eurekahedge Japan Hedge Fund Index |

(6.17%) |

12.91% |

5.39% |

Eurekahedge Greater China Hedge Fund Index |

(11.47%) |

29.97% |

13.61% |

Eurekahedge India Hedge Fund Index |

(6.83%) |

27.60% |

6.63% |

Eurekahedge Australia/New Zealand Hedge Fund Index |

(3.47%) |

7.11% |

10.30% |

Eurekahedge Emerging Markets Hedge Fund Index |

(3.93%) |

16.96% |

11.21% |

Eurekahedge Latin American Hedge Fund Index |

7.82% |

13.71% |

13.08% |

Source: Eurekahedge

Table 2: Strategy indices performance

| Index |

2018 YTD Return |

2017 Return |

Annualised Return |

|---|---|---|---|

Eurekahedge Arbitrage Hedge Fund Index |

1.74% |

5.28% |

6.91% |

Eurekahedge CTA/Managed Futures Hedge Fund Index |

(4.20%) |

2.27% |

8.56% |

Eurekahedge Distressed Debt Hedge Fund Index |

4.59% |

6.68% |

10.45% |

Eurekahedge Event Driven Hedge Fund Index |

0.93% |

10.16% |

9.25% |

Eurekahedge Fixed Income Hedge Fund Index |

0.40% |

6.60% |

7.58% |

Eurekahedge Long Short Equities Hedge Fund Index |

(3.61%) |

12.90% |

8.24% |

Eurekahedge Macro Hedge Fund Index |

(2.26%) |

4.20% |

7.69% |

Eurekahedge Multi-Strategy Hedge Fund Index |

(2.34%) |

9.19% |

8.93% |

Eurekahedge Relative Value Hedge Fund Index |

2.39% |

6.82% |

8.86% |

CBOE Eurekahedge Long Volatility Hedge Fund Index |

(4.38%) |

(10.95%) |

4.13% |

CBOE Eurekahedge Relative Value Volatility Hedge Fund Index |

(1.36%) |

3.23% |

8.41% |

CBOE Eurekahedge Short Volatility Hedge Fund Index |

(8.08%) |

9.06% |

7.54% |

CBOE Eurekahedge Tail Risk Hedge Fund Index |

(5.36%) |

(14.22%) |

(5.48%) |

Eurekahedge Equity Long Bias Hedge Fund Index |

(4.64%) |

17.00% |

8.83% |

Eurekahedge Equity Market Neutral Hedge Fund Index |

(1.68%) |

3.85% |

5.02% |

Eurekahedge Trend Following Index |

(7.98%) |

0.34% |

9.21% |

Eurekahedge FX Hedge Fund Index |

0.39% |

(0.19%) |

7.38% |

Eurekahedge Commodity Hedge Fund Index |

(5.64%) |

1.27% |

9.27% |

Eurekahedge Crypto-Currency Hedge Fund Index |

(64.90%) |

1,708.50% |

128.36% |

Eurekahedge AI Hedge Fund Index |

(5.27%) |

8.70% |

8.62% |

Eurekahedge ILS Advisers Index |

(2.13%) |

(5.60%) |

4.75% |

Source: Eurekahedge

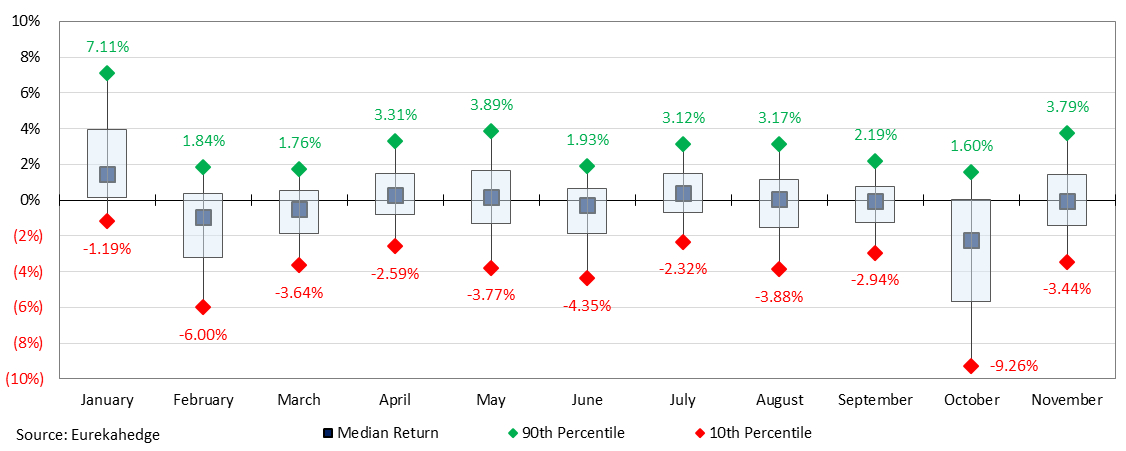

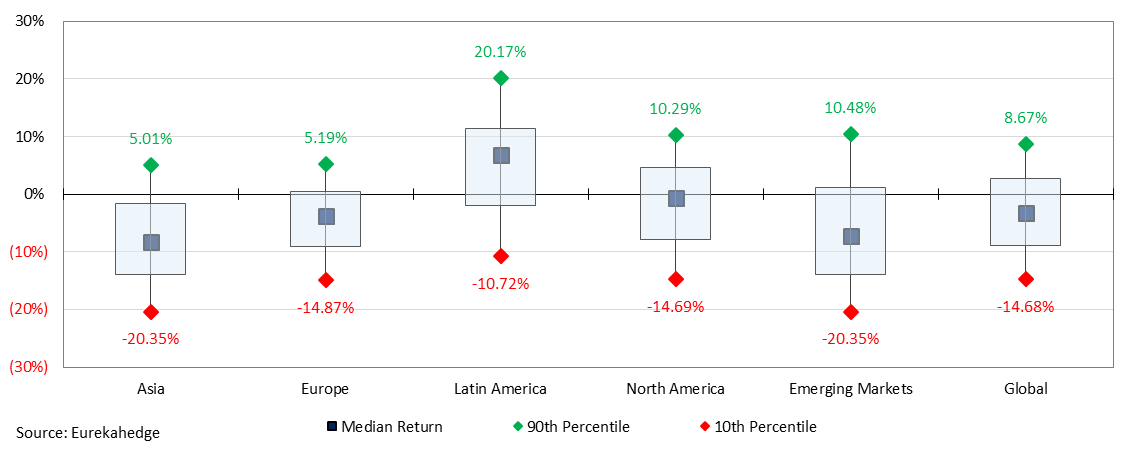

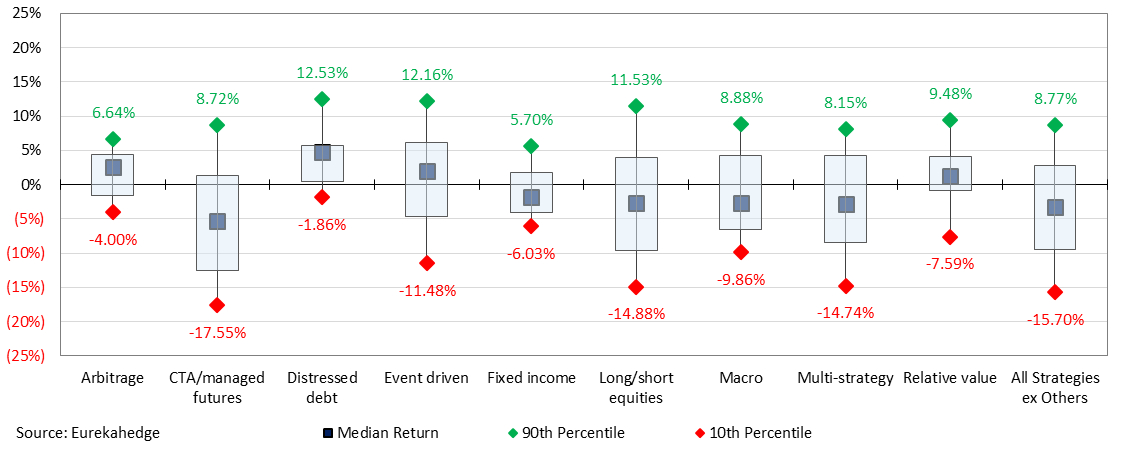

The following three figures provide the performance distribution of hedge fund managers tracked by Eurekahedge throughout the year 2018. The difficult trading situation and various challenges faced by the industry has allowed exceptional hedge fund managers to distinguish themselves from the rest of their peers by proving that they were able to generate good returns amidst the market downturn. A bad year for the industry tends to be a good opportunity for investors to identify qualifying fund managers.

Figure 1a: 2018 monthly returns distribution of the global hedge fund industry

Figure 1b: 2018 year-to-date returns distribution across geographic mandates

Figure 1c: 2018 year-to-date returns distribution across strategic mandates

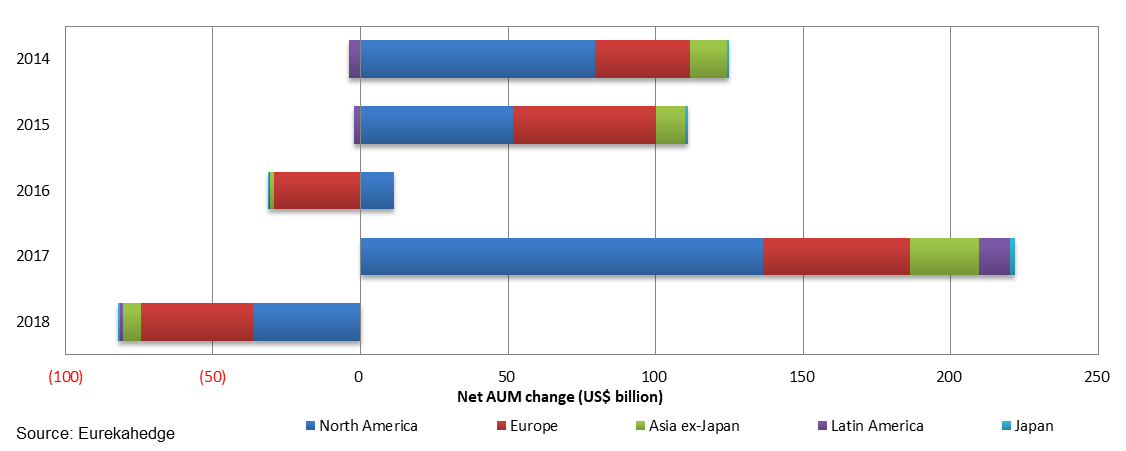

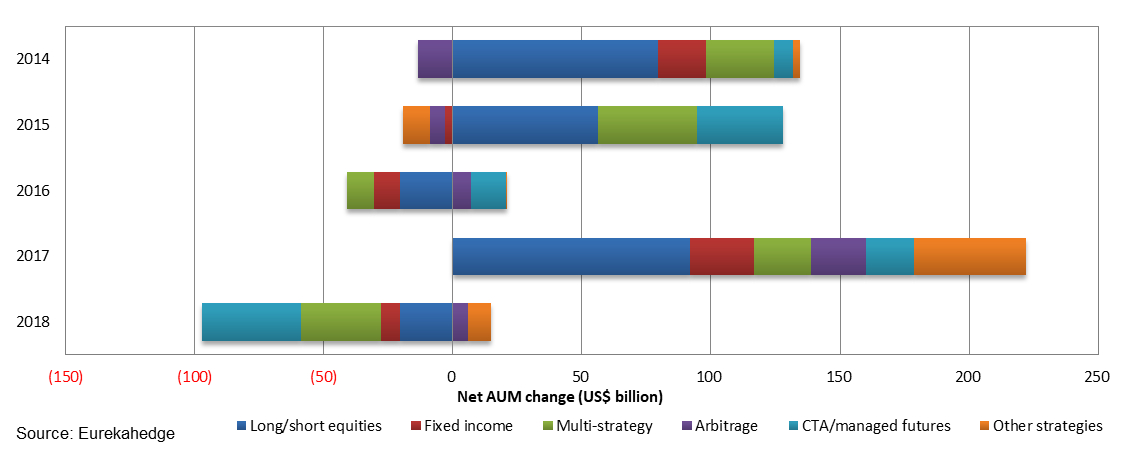

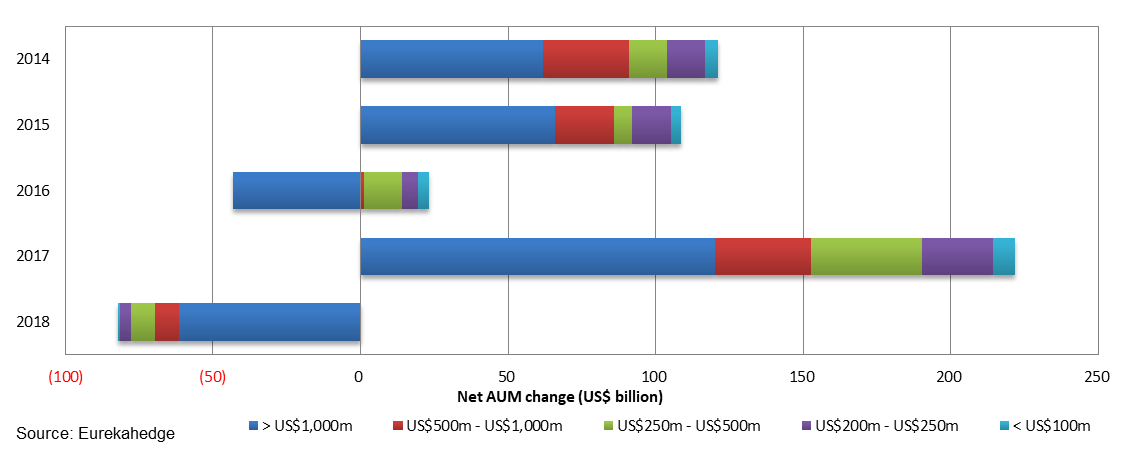

Figures 2a-2c provide the breakdown of asset flows within the global hedge fund industry, broken down across geographies, strategies, as well as fund sizes over the last few years. None of the major regions saw net increase in AUM throughout the year, and most of the strategic mandates were also in the red year-to-date. Billion dollar funds have continued to account for the largest portion of asset flows, be it positive or negative over the recent years.

Figure 2a: Net AUM change by geographic mandate

Figure 2b: Net AUM change by strategic mandate

Figure 2c: Net AUM change by fund size

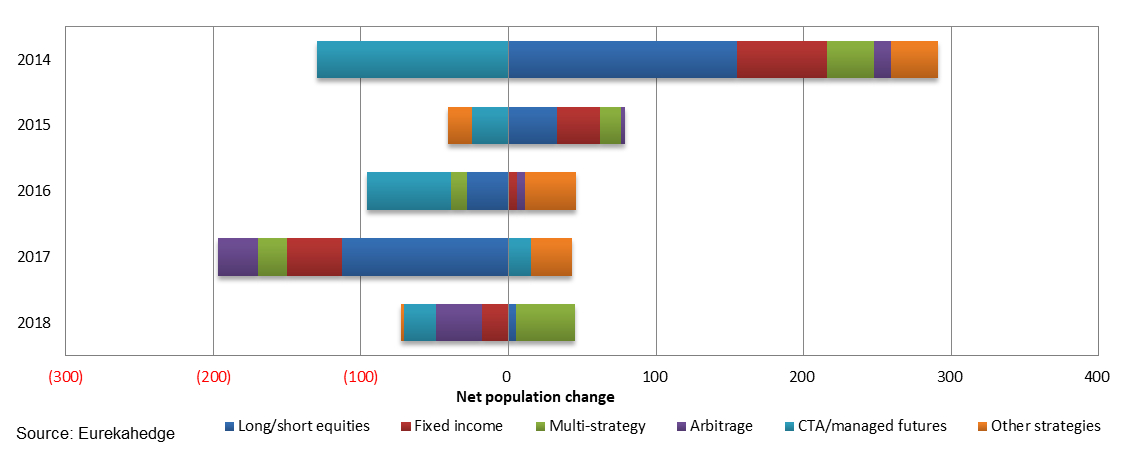

Figures 3a-3b illustrate population changes across regions and strategies over the last few years. The high attrition rate among small hedge funds within the European region has continuously exerted pressure on the European hedge fund industry’s population since 2015. On the other end, Asian hedge fund industry has seen net increases in their population since 2014. In 2018 alone, there are estimated to be 45 more launches than closures within the Asia ex-Japan region, indicating strong demands among investors for exposure toward Asian assets, despite all the challenges faced by fund managers in the region.

Figure 3a: Net population change by geographic mandate

A similar breakdown is seen in Figure 3b across major strategic mandates. Long/short equities have seen population growth slowing down, as interest levels for less common investing strategies have risen among investors over the past few years.

Figure 3b: Net population change by strategic mandate

Tables 3a-3b provide the hedge fund management and performance fee averages based on launch year and geographic mandate. Generally, apart from certain outliers, the industry has witnessed a trend of fee decline over the last decade as growing competition from other investment vehicles and consistent single-digit yearly returns post-financial crisis have drawn investors’ scrutiny, raising questions whether average hedge fund managers deserve their ‘expensive’ fees.

Table 3a: Average hedge fund management fees across geographic mandates

| Launch Year |

North America |

Europe |

Asia |

Latin America |

Global |

|---|---|---|---|---|---|

2006 |

1.63% |

1.56% |

1.60% |

1.76% |

1.60% |

2007 |

1.74% |

1.51% |

1.63% |

2.01% |

1.63% |

2008 |

1.56% |

1.47% |

1.60% |

1.77% |

1.52% |

2009 |

1.61% |

1.46% |

1.67% |

1.63% |

1.54% |

2010 |

1.62% |

1.53% |

1.60% |

1.69% |

1.56% |

2011 |

1.63% |

1.44% |

1.61% |

1.58% |

1.51% |

2012 |

1.53% |

1.38% |

1.55% |

1.74% |

1.46% |

2013 |

1.49% |

1.24% |

1.39% |

1.80% |

1.34% |

2014 |

1.48% |

1.28% |

1.48% |

1.57% |

1.35% |

2015 |

1.48% |

1.16% |

1.49% |

1.85% |

1.29% |

2016 |

1.38% |

1.27% |

1.41% |

1.32% |

1.30% |

2017 |

1.41% |

1.10% |

1.45% |

1.38% |

1.23% |

2018 |

1.39% |

1.24% |

1.73% |

1.17% |

1.31% |

Source: Eurekahedge

Table 3b: Average hedge fund performance fees across geographic mandates

| Launch Year |

North America |

Europe |

Asia |

Latin America |

Global |

|---|---|---|---|---|---|

2006 |

18.97% |

17.18% |

18.24% |

19.26% |

18.05% |

2007 |

19.71% |

16.70% |

17.96% |

18.57% |

18.04% |

2008 |

18.45% |

15.94% |

17.76% |

18.23% |

17.17% |

2009 |

18.39% |

15.82% |

17.28% |

17.50% |

17.01% |

2010 |

18.06% |

16.26% |

18.85% |

17.96% |

16.92% |

2011 |

18.38% |

15.90% |

17.59% |

15.69% |

16.77% |

2012 |

17.69% |

15.24% |

17.55% |

17.12% |

16.23% |

2013 |

16.98% |

13.52% |

16.43% |

18.70% |

14.91% |

2014 |

16.27% |

14.54% |

17.04% |

15.47% |

15.29% |

2015 |

15.56% |

13.55% |

17.24% |

19.17% |

14.48% |

2016 |

17.50% |

13.93% |

18.67% |

16.60% |

15.14% |

2017 |

18.23% |

14.55% |

16.55% |

15.00% |

15.54% |

2018 |

15.71% |

15.13% |

18.25% |

18.33% |

15.37% |

Source: Eurekahedge

The full article inclusive of all charts and tables is available in The Eurekahedge Report accessible to paying subscribers only.

Subscribers may continue to login as usual to download the full report and non-subscribers may email database@eurekahedge.com to enquire on how to obtain the full research report