|

|

Indices

Index Flash Update - 09 June 2022

EQUAL WEIGHTED HEDGE FUND INDICES

ASSET WEIGHTED HEDGE FUND INDICES

SPECIALIST ALTERNATIVE FUND INDICES

INVESTIBLE BENCHMARK INDICES

METHODOLOGIES

INDEX PRESS RELEASES

- Index Flash Update (June 2022)

- Index Flash Update (May 2022)

- Index Flash Update (April 2022)

- Eurekahedge launches new benchmark Eurekahedge Multi-Factor Risk Premia Index

- Eurekahedge and CBOE launch four benchmark indices tracking volatility-based investment strategies

- Eurekahedge and MPI announce new benchmark index tracking the top 50 hedge funds

- Eurekahedge and ILS Advisers launch new USD hedge index

- Eurekahedge launches new insurance linked securities index

- Eurekahedge Asset Weighted Index goes live

- Eurekahedge Asset Weighted Index press release

- EU Benchmark Regulation

| Hedge funds fell for a second straight month in May amid rising uncertainty over geopolitical and economic tensions |

|---|

|

The Eurekahedge Hedge Fund Index declined -0.52% in May 2022, trailing behind the S&P 500 which eked out a 0.01% return over the same period. Widespread investor caution and uncertainty over both geopolitical and economic tensions continued to linger as inflation remains persistently high amid the ongoing Russia-Ukraine war and continued global supply chain disruptions. This has fanned concerns that the Federal Reserve will be forced to tighten monetary policy more aggressively to prevent inflation from spiralling out of control and at the same time avoid pushing the economy into a recession. Market participants are expecting the Federal Reserve to hike interest rates by 50bps in its June and July meetings and then move to a more modest 25bps for the rest of 2022. Compounding matters further, the BA.4 and BA.5 Omicron subvariants which are better than previous versions of Omicron at evading the immune system’s defences are steadily gaining ground, adding more uncertainty to the future trajectory of the global coronavirus pandemic. Over in Europe, returns were mixed among equity benchmarks in the region with the RTS Index up 11.71% while the Euro Stoxx 50 and CAC 40 Index were down -0.36% and -0.99% respectively. The high prices for commodities, which is Russia’ key source of revenue combined with the imposition of capital controls has enabled the Russian rouble to appreciate by a further 14.29% against the US dollar in May, supporting the performance of the RTS Index. Returns were negative across geographic mandates in May, except for the Latin American mandate which posted a return of 0.88% while the Japanese mandate trailed behind their peers with a return of -1.50%. Across strategies, the macro mandate performed the best, posting the smallest decline of -0.11% while the event driven mandate trailed behind their peers with a return of -1.55%. Roughly 38.6% of the underlying constituents of the Eurekahedge Hedge Fund Index posted positive returns in May, and 43.0% of the hedge fund managers in the database were able to maintain a positive return in 2022. |

| Below are the key highlights for the month of May 2022 |

|---|

|

| Index of the Month |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Latin American Hedge Fund Index | 0.88 | 4.20 | -1.33 |

Main Indices

| Main Eurekahedge Indices |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Hedge Fund Index | -0.52 | -2.61 | 9.56 |

| Eurekahedge Fund of Funds Index | -0.55 | -4.11 | 8.53 |

| Eurekahedge Long-only Absolute Return Fund Index | -1.21 | -9.77 | 12.71 |

Regional Indices

| Eurekahedge Regional Indices |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge North American Hedge Fund Index | -0.13 | -3.92 | 13.52 |

| Eurekahedge European Hedge Fund Index | -1.24 | -5.94 | 9.04 |

| Eurekahedge Japan Hedge Fund Index | -1.50 | -5.18 | 8.70 |

| Eurekahedge Emerging Markets Hedge Fund Index | -0.12 | -4.38 | 2.43 |

| Eurekahedge Asia ex Japan Hedge Fund Index | -1.47 | -9.21 | 7.72 |

| Eurekahedge Latin American Hedge Fund Index | 0.88 | 4.20 | -1.33 |

Returns were negative across regional mandates in May, with the Latin American mandate the only exception as it posted a return of 0.88%, supported by the positive performance of the Latin American equity market as the Brazil IBOVESPA and IPC Mexico returned 3.22% and 0.65% respectively. Meanwhile, the North American mandate ended May with a slight decline of -0.13% while the European and Asia ex-Japan mandates posted steeper losses of -1.24% and -1.47% respectively.

Strategy Indices

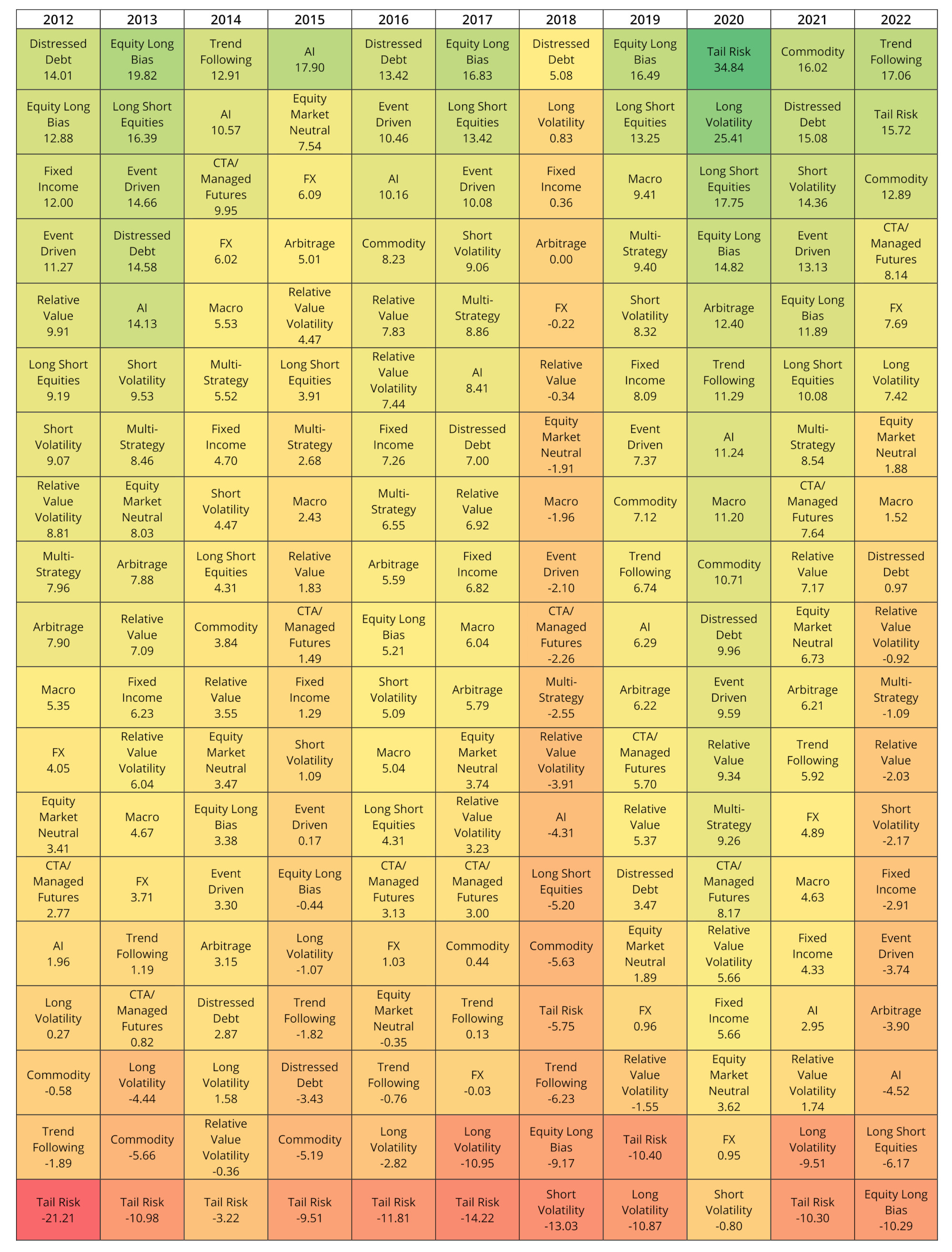

Returns were negative across strategic mandates in May, with the event driven and arbitrage mandates posting the sharpest losses of -1.55% and -1.23% respectively. On the other end of the spectrum, the macro, distressed debt and CTA/Managed Futures mandates posted relatively smaller losses of -0.11%, -0.19% and -0.20% respectively. Despite the negative performance in May, the CTA/Managed Futures mandate remains the best performer in 2022 with a return of 8.14% while the macro mandate came in a distant second with a return of 1.52%.

Table 1: Strategy return map

| Eurekahedge Strategy Indices |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Arbitrage Hedge Fund Index | -1.23 | -3.90 | 6.21 |

| Eurekahedge CTA/Managed Futures Hedge Fund Index | -0.20 | 8.14 | 7.64 |

| Eurekahedge Distressed Debt Hedge Fund Index | -0.19 | 0.97 | 15.08 |

| Eurekahedge Event Driven Hedge Fund Index | -1.55 | -3.74 | 13.13 |

| Eurekahedge Fixed Income Hedge Fund Index | -0.80 | -2.91 | 4.33 |

| Eurekahedge Long Short Equities Hedge Fund Index | -0.26 | -6.17 | 10.08 |

| Eurekahedge Macro Hedge Fund Index | -0.11 | 1.52 | 4.63 |

| Eurekahedge Multi-Strategy Hedge Fund Index | -0.30 | -1.09 | 8.54 |

| Eurekahedge Relative Value Hedge Fund Index | -0.31 | -2.03 | 7.17 |

| CBOE Eurekahedge Long Volatility Hedge Fund Index | -0.81 | 7.42 | -9.51 |

| CBOE Eurekahedge Relative Value Volatility Hedge Fund Index | 1.21 | -0.92 | 1.74 |

| CBOE Eurekahedge Short Volatility Hedge Fund Index | 0.22 | -2.17 | 14.36 |

| CBOE Eurekahedge Tail Risk Hedge Fund Index | -0.18 | 15.72 | -10.30 |

| Eurekahedge Equity Long Bias Hedge Fund Index | -1.27 | -10.29 | 11.89 |

| Eurekahedge Equity Market Neutral Hedge Fund Index | 0.45 | 1.88 | 6.73 |

| Eurekahedge Trend Following Index | -0.74 | 17.06 | 5.92 |

| Eurekahedge FX Hedge Fund Index | -0.23 | 7.69 | 4.89 |

| Eurekahedge Commodity Hedge Fund Index | -1.87 | 12.89 | 16.02 |

| Eurekahedge Crypto-Currency Hedge Fund Index | -22.62 | -40.14 | 142.25 |

| Eurekahedge AI Hedge Fund Index | -0.30 | -4.52 | 2.95 |

| Eurekahedge ILS Advisers Index | 0.00 | 0.33 | 1.04 |

| Eurekahedge Global Hedge Fund Indices by Fund Size |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Small Hedge Fund Index (< US$100m) | -0.35 | -2.25 | 9.99 |

| Eurekahedge Medium Hedge Fund Index (US$100m - US$500m) | -0.50 | -2.49 | 8.51 |

| Eurekahedge Large Hedge Fund Index (> US$500m) | -0.71 | -0.91 | 8.72 |

| Eurekahedge Billion Dollar Hedge Fund Index | -0.45 | -0.15 | 8.16 |

| Eurekahedge Asset Weighted Indices |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Asset Weighted Index – USD | -0.35 | -1.89 | 4.06 |

| Eurekahedge TOP100 Asset Weighted Index – USD | -0.29 | -0.18 | 3.54 |

| Eurekahedge TOP300 Asset Weighted Index - USD | -0.37 | -1.11 | 4.08 |

| Asia-Eurekahedge Indices |

May 2022* |

2022 Returns | 2021 Returns |

|---|---|---|---|

| Eurekahedge Greater China Hedge Fund Index | -1.16 | -12.61 | 2.98 |

| Eurekahedge India Hedge Fund Index | -7.65 | -12.29 | 26.89 |

Click here to download our daily indices for free. Our indices are updated with the latest fund returns at 23:30 GMT every day and we encourage you to use them to benchmark your portfolio or fund performance. If you would like us to create a bespoke index for you, please let us know.